SEC’s Rule 6c-11 Impact on the Tax Efficiency of ETFs

Posted on Feb 19, 2022Maddie White

I. ETF Operations

An ETF is a fund that holds a basket of securities, and shares of the ETF, rather than the securities themselves, that can be bought and sold on an exchange.[1] The basket of securities tracks an outside benchmark, usually an index.[2] The innovation of ETFs is their dual trading system, in which ETF shares trade on stock exchanges like a typical stock; but, the number of ETF shares can also grow or shrink through creations/redemptions in the primary market by investors known as authorized participants (APs).[3] To create shares of an ETF, an AP provides a fund with a basket of securities(the “creation basket”) that make up the index the fund follows.[4] In exchange, it receives shares of the ETF.[5] To redeem shares, an AP returns shares to the fund.[6] The AP will receive an “in-kind” redemption from the fund, which is a basket of securities (“redemption basket”) that make up the underlying index.[7] This process is important because it keeps the price of ETF shares in line with the underlying value of the stocks it holds.[8]

II. ETF Taxation and the “Heartbeat” Trade

When ETFs engage in a creation/redemption transaction, they do not recognize a gain from distributing appreciated securities to APs under 26 U.S.C. § 852(b)(6).[9] This exemption allows ETFs to get rid of securities with the highest unrealized gains through in-kind redemptions,[10] which makes ETFs tax efficient vehicles that rarely distribute capital gains to investors.[11]

However, sometimes an ETF is forced to rebalance or remove a stock from its portfolio because of a change in the index it tracks.[12] In such cases, there may not be enough in-kind transactions to remove the appreciated stock from its portfolio by the needed date.[13] In these situations, an ETF will often engage in a practice known as “heartbeat trade.”[14] In a “heartbeat trade”, a fund will receive a large influx of capital from an AP, usually a bank, to create fund shares.[15] Within a few days, the same bank will remove its capital by redeeming its newly created shares.[16] This process is aimed specifically to transfer out appreciated securities in the in-kind redemption basket, which will wash out any capital gains.[17] In recent years, these trades have received a significant amount of coverage as Wall Street’s “dirty little secret”[18] that allows ETFs to avoid taxes.[19] The trades have been growing over the years, with Bloomberg finding that there were 548 such trades in 2018 worth an estimated $98 billion.[20]

Heartbeat trades have caused debate about their legality and fairness.[21] Unlike typical in-kind redemptions, these transactions are generated by the portfolio manager rather than the demand of fund shareholders.[22] This has caused some to argue that the trades are “sham transactions” undertaken only for tax avoidance.[23] Such arguments are bolstered by the language of § 852(b)(6), which exempts in-kind redemptions only if they are “upon the demand of the shareholder.”[24] Despite the controversy and their increased use the IRS has yet to comment on heartbeat trade legality, only noting it is aware of the existence.[25]

III. SEC Rule 6c-11

In 2019, the SEC promulgated Rule 6c-11[26] to standardize the operation of ETFs.[27] Importantly, the rule allows all ETFs to use “custom baskets,” which are “baskets that do not reflect: (i) a pro rata representation of the ETF’s portfolio holdings.”[28] Prior to 6c-11, only certain funds formed in 2006 or earlier had to been able to use custom baskets.[29]Funds formed after 2006 were required to issue baskets that corresponded pro rata to their holdings.[30]

IV. Evaluation of Rule 6c-11’s Impact

The promulgation of Rule 6c-11 has the potential to increase the use of heartbeat trades because all funds now have greater flexibility to assemble baskets that are heavy in appreciated stocks, even if the basket is not representative of its underlying index.[31]

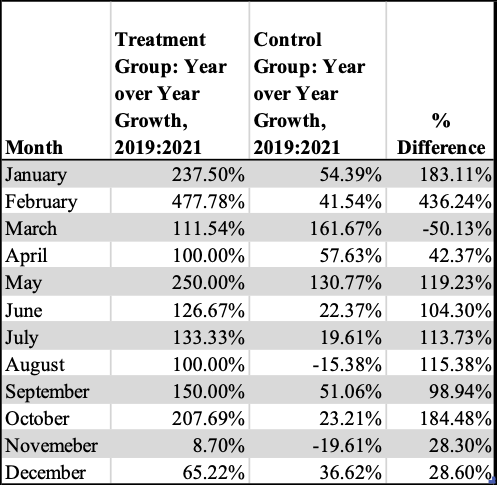

In order to evaluate whether this is true, I split the ETF universe into funds that had custom basket access (“control group”) and those that gained it after 6c-11 went into effect (“treatment group”). Following the method of Moussawi et. al., I was able to identify when funds engaged in heartbeat trades by evaluating the flow of assets into ETFs.[32] I compared the growth in heartbeat trades between 2019 and 2021[33] for both groups, presented in Table 1.

Table 1: YOY Growth in Heartbeat Trades

In all months except March, the growth in heartbeat trades in the “treatment group” is greater, with a maximum difference of 436%. Thus, there has been a pronounced increase in the usage of heartbeat trades following the implementation of Rule 6c-11, and the increase was larger for funds that were not able to use custom baskets before the adoption of the rule. Although these results do not shed light on the legality of such trades, they do show that heartbeat trades are growing as a result of SEC action and will continue to grow now that all funds have a tool to increase the efficacy of such trades. Given this growth, the IRS should no longer avoid the issue and should explicitly rule on its view of their legality as their frequency and scale will only continue to grow.

____________________

[1] State Street Global Advisors, What Is an ETF?, https://www.ssga.com/us/en/intermediary/etfs/resources/education/what-is-an-etf.

[2] See Laurent Deville, Exchange Traded Funds: History, Trading, and Research, Handbook of Financial Engineering, 67, 67 (2008).

[3] Id. at 76.

[4] Id.

[5] Id. at 77–78.

[6] Id.

[7] See Joanne m. hill et al, A comprehensive guide to exchange-traded funds (ETFs) 11, 24 (CFA Institute Research Foundation) (2015), http://www.cfapubs.org/doi/pdf/10.2470/rf.v2015.

[8] See id. at 24.

[9] 26 U.S.C. § 852(b)(6) (“Section 311(b) shall not apply to any distribution by a regulated investment company to which this part applies, if such distribution is in redemption of its stock upon the demand of the shareholder.”); 26 U.S.C.A. § 311(b) (“In general If(A)a corporation distributes property. . . to a shareholder in a distribution to which subpart A applies, and(B)the fair market value of such property exceeds its adjusted basis. . . gain shall be recognized to the distributing corporation as if such property were sold to the distributee at its fair market value.”).

[10] Rabih Moussawi et al., ETF Heartbeat Trades, Tax Efficiencies, and Clienteles: The Role

of Taxes in the Flow Migration from Active Mutual Funds to ETFs, (December 8, 2020), available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3744519.

[11] See Ben Johnson, ETFs Again Proved Their Worth to Taxable Investors in 2020, Morningstar (Dec. 15, 2020), https://www.morningstar.com/articles/1014538/etfs-again-proved-their-worth-to-taxable-investors-in-2020 (noting that “Exchange-traded funds aren’t impervious to distributing capital gains, but most have avoided them.”).

[12] See Elisabeth Kashner, The Heartbeat of ETF Tax Efficiency, FACTSET (Dec. 18, 2017), https://insight.factset.com/the-heartbeat-of-etf-tax-efficiency [https://perma.cc/RH88-8XSZ].

[13] See id.

[14] See id.

[15] See id.; See also Zachary R. Mider et al., The ETF Tax Dodge Is Wall Street’s ‘Dirty Little Secret’, Bloomberg (Mar. 29, 2019), https://www.bloomberg.com/graphics/2019-etf-tax-dodge-lets- investors-save-big/ [https://perma.cc/VY83-C85B].

[16] See Kashner, supra note 12.

[17] Id.

[18] See Mider et. al, supra note 15.

[19] See id.

[20] See id.

[21] See Mider et al., supra note 15 (quoting Jeffrey Colon, a tax professor; “the transactions may be vulnerable to an IRS challenge.”).

[22] See Kashner, supra note 12.

[23] See Mider et al., supra note 15 (quoting Peter Kraus; “If the IRS were looking at it, they would say that’s a sham transaction.”); See Kashner, supra note 12 (noting that tax deferral is the only function of a heartbeat trade that cannot be replicated by different trade type).

[24] § 852(b)(6).

[25] See Mider et al, supra note 12.

[26] See 17 C.F.R. § 270.6c-11 (“Rule 6c-11”); Exchange-Traded Funds, Investment Company Act Release No. 33-10695, at 9 (Dec. 23, 2019)(to be codified at 17 C.F.R. pts. 210, 232, 239, 270, and 274), https://www.sec.gov/rules/final/2019/33-10695.pdf [hereinafter SEC Final Rule].

[27] Press Release, SEC, SEC Adopts New Rule to Modernize Regulation of Exchange-Traded Funds (Sept. 26, 2019), https://www.sec.gov/news/press-release/2019-190.

[28] See SECFinal Rule, supra note 21, at 90-91.

[29] See id. at 82.

[30] See id. at 83.

[31] Saqib Iqbal Ahmed, SEC adopts new rules to level playing field for ETF provider, Reuters (Sept. 26, 2019), https://www.reuters.com/article/us-usa-sec-etf/sec-adopts-new-rules-to-level-playing-field-for-etf-providers-idUSKBN1WB2JG

[32] See Moussawu et. al., supra note 10, at 17.

[33] 2019 was chosen as the comparison year because the SEC rule went into effect Dec. 22, 2019 but compliance was not required until Dec 23., 2020. During the interim period, it is not possible to tell which funds operated under Rule 6c-11. See Final SEC Final Rule, supra note 21.